The Financial Abuse of Mary by RBS/NatWest

Background

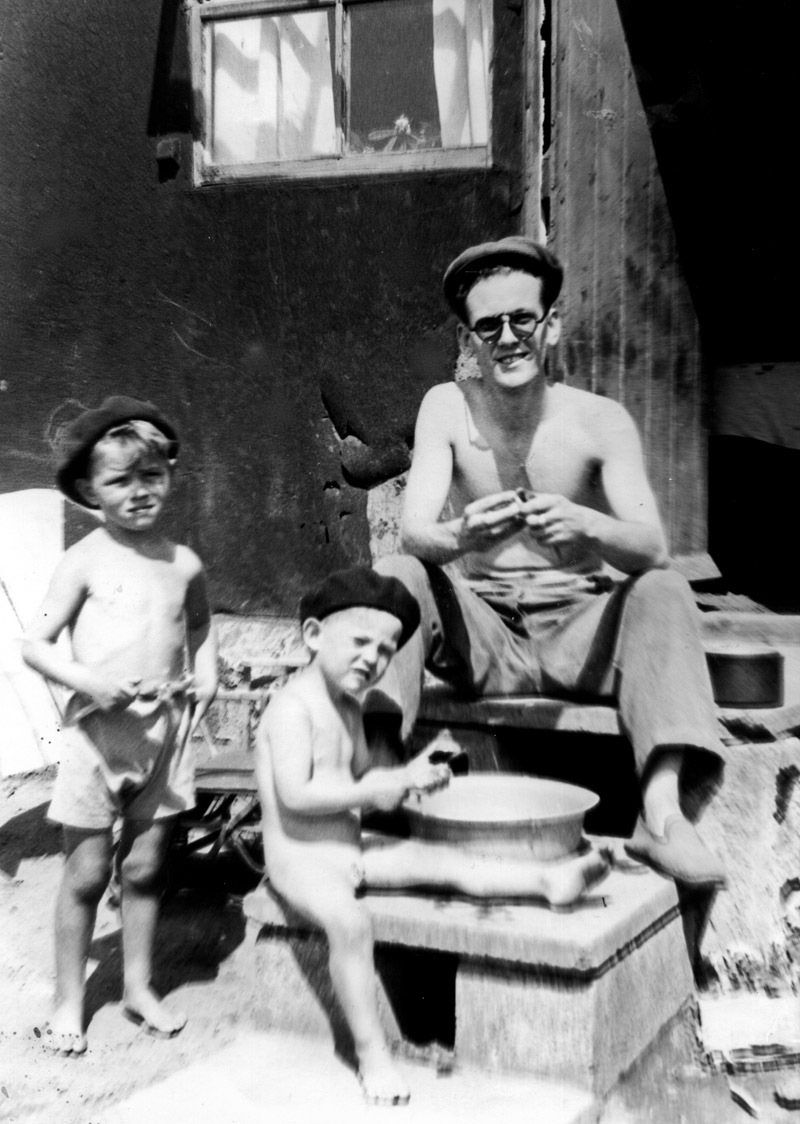

At the age of 12 my dad worked down a pit in the Rhondda Valley, South Wales. He was carried up to the pithead in the dark in the morning by his father and down again in the dark at night. At 17 he met my mother in Birmingham and cycled from south Wales to the Midlands at weekends just to see her. He enlisted when WW2 started and married my mother Mary who worked long hours in a munitions factory. At the end of WW2 no homes were available for returning servicemen and their families so my parents, and my brother and I were forced to live in a wooden chicken shed in a field just outside Birmingham. It was primitive. I remember shaking with cold during the winter months. We got bye with a simple wooden table, metal plates billy cans and a small primus stove. We only had two plain hairy grey blankets each smelling of damp to keep us warm at night. The floor was grass and the roof leaked. 1947 was bloody cold. We wore layers of other people’s caste off clothes or no clothes. Other families arrived and a basic toilet block and washing facilities were organised. A small working-class community evolved and friendships formed that lasted a lifetime.

|

|

| Our family’s humble beginnings | RBS/NatWest’s not so humble beginnings |

After 3 years we moved to a rundown council estate in south Birmingham. Post war rationing and limited income necessitated careful spending and a ‘save’ mentality. My father was a modest shy man with strong principles, strict yet kind. My classmates told of how their fathers had been at Dunkirk and asked me, “What did your dad do during the war?”. I asked my dad and he replied, “Nobody wins in war son” and then silence, he didn’t want to talk about it. When he was in his eighties, I was clearing out one of his draws and came across a bunch of medals in a box. I asked what they were for and he reluctantly told me he was a pilot in the Fleet Air Arm and had seen active service in the Atlantic, North Sea, and D-day. He had lost many close friends and been shot down twice himself. He was probably mentally damaged by his war experiences.

My parents loved me and I loved them. My father continued to serve his country by dedicating himself to the most important profession in the world – education. After retirement as a family, we emigrated to a small town in New Zealand. They valued the friendship Kiwis showered on them and often spoke enthusiastically about equality that was enshrined in the country – something they thought was missing in UK society. My parents became well known and respected in the town and were referred to as ‘the honeymoon couple’ because they were clearly in love even after 73 years of marriage.

My father died in October 2015 aged 92 years. I was fortunate to be able to sit with him in the hospital during his last days. He’d lived a fulfilling life but at the end he only wanted talk about how best to support my mother after he was gone. I promised him I would keep mum safe despite her disability – she had developed dementia in her early 80s and lacked mental capacity. We had prepared for this moment. I had Probate for my father’s will, issued by the High Court in New Zealand, and Enduring Power of Attorney for my mother also issued by a New Zealand court. These, we hoped, enabled me to inform his UK based work related pension fund ‘Teachers Pensions’ of his death and to activate my mother’s widow’s benefit from his pension.

Enduring Power of Attorney issued in New Zealand is not recognised by legal bodies in the UK. This can cause problems since many UK citizens move to colonial countries like Australia, New Zealand, Canada and access pensions in the UK. The UK Government’s Leeds Probate Office accepted the sealed Probate document issued in the High Court in New Zealand. New Zealand is a Country recognised by the UK under the UK’s Colonial Probates Act, which means a Grant of Probate issued by the High Court in Zealand can be resealed by the Probate Registry in the UK.

I’m ashamed to say I failed to keep my mother safe

My mother, aged 92 years, was provided with a widow’s pension from my father’s UK based work related pension ‘Teachers Pensions’. They were very thorough, efficient, and rigorous, in checking I had all my parent’s original documents e.g. birth certificates, marriage certificates, my father’s death certificate. Teachers Pensions accepted that I had Probate for my father’s will and Enduring Power of Attorney for my mother and agreed to pay the widow’s pension due to my mother but only into a UK bank that I nominated. Any name and any bank they said was OK. So, I could have opened an account in my name only. If I had I wouldn’t be writing this sad story. I asked the Office of the Public Guardian (OPG) for help thinking I needed to ensure my mum would be protected if I opened an account in my name only. The OPG are sponsored by the Ministry of Justice to keep vulnerable people safe. They suggested, for the sake of transparency, that I open a joint account, in my name and my mother’s name in the bank where I already had a bank account i.e. NatWest. So that is what I did. It was a big mistake that led to great pain for my mother and for me.

In November 2015 I contacted my own local bank NatWest and arranged to meet with the manager Mr Rose. I made it very clear that that, on the advice of the Office of the Public Guardian, I wanted to open an account in my name and my mother’s name and my name. I provided Mr Rose with all the documents he required including the New Zealand Probate for my father’s will and Enduring Power of Attorney document issued by a New Zealand court for my mother. Mr Rose needed my mother’s address in New Zealand. I supplied this on the understanding that my mother had dementia and unable to manage her own affairs and was not, under any circumstances, to be contacted by the Bank.

Being very cautious I asked for a second meeting with Mr Rose. He said he’d checked with NatWest Bank’s ‘Power of Attorney Team’ in Kent. He told me there were no problems my arranging to pay money from Teachers Pensions into the account or for me to have access to the account in order to send it to my mother’s account in New Zealand. Mr Rose even contacted the ‘Power of Attorney Dept’ in Kent and by phone call with me present to confirm the Bank’s acceptance. He opened the account for me with me sitting next to him providing details. I received a letter from NatWest dated 16th November 2015 stating the account in both our names was open and functioning. On my direction Teacher’s Pension UK began paying money into our joint NatWest account on 4th December 2015. They deposited a lump sum followed by smaller monthly sums and this was shown in NatWest Bank statements sent to me.

However, in late February 2017, I received a letter from NatWest’s ‘Power of Attorney Team’ in Kent ‘rubber stamped’ by the Head of Customer Services. The letter was dated ‘17th November 2016. The letter informed me that NatWest did not recognise a New Zealand Power of Attorney. Hence, to my dismay, I was realised that NatWest had opened an account in my mother’s name only, without her permission (or mine), and that the money I had deposited, £3,372.21, was now the sole property of NatWest Bank.

Trying to find a solution

NatWest’s letter did not accept or apologise for the mistake they made. It suggested I contact any NatWest branch to discuss the matter or ring the Bank’s helpline. I arranged a meeting with Mr Rose the local branch manager only to be told he’d been sacked. The new manager apologised for the Bank’s mistake but was unable to suggest a way forward. I had hoped NatWest would have been more proactive in solving a problem of its own making.

I phoned the bank’s helpline three times, but no solution was offered. They suggested I could seek legal advice but added that NatWest were unable to meet any costs arising whilst agreeing that NatWest were at fault. My suggestion that NatWest return the money to Teachers Pensions was not an option, they claimed.

I realised NatWest’s approach – to kick the problem into the long grass – was a common strategy often employed by large organisations. The ensuing bureaucratic nightmare is designed to destroy the will of complainants.

The pain and suffering that followed.

I was contacted by the manager of my mother’s Care Home in New Zealand, to tell me that my mother was greatly distressed. Her blood pressure and heart rate were high; she was sweating and her heart pounding. The Manager explained that my mother became anxious on hearing that her bank account in the UK was frozen and her funds not accessible to her. NatWest had contacted my mother when I expressly told them not to. The highlight of my mom’s week was to go out with staff to have coffee at a local cafe. This stopped because my mother didn’t want to go out anymore – “I don’t have any money”. My parents never owed money; they bought what they needed not what they wanted; they were frugal, always. I was angry at NatWest Bank and worried for my mother’s mental and physical health.

I rushed to New Zealand in April 2017 to ensure that my mother’s finances and Care Home provision were sufficient to her changing needs and most importantly to alleviate my mother’s anxiety given her fragile mental health. I met with the Care Home Manager and staff to discuss how to protect my mother from future NatWest communication. Sadly, the anxiety continued and she had to be moved to another Care Home with hospital facilities which incurred increased costs. Her doctor stressed the importance of stopping all communication from RBS/NatWest.

The money in the account I set up in our joint names, a sum of £3372.21, was only accessible to RBS/NatWest. I contacted Teachers Pensions and explained the problem caused by RBS/NatWest Bank and asked for any outstanding money to be transferred to an account in my name only, in another bank is not NatWest. This was carried out quickly and efficiently by Teachers Pensions and I was able to transfer the money to my mother’s account in New Zealand in March 2017.

The RBS/NatWest Bank made no attempt to resolve the problem of its own making which had far reaching ramifications for my mother and me. I had no option but to make a formal complaint to NatWest in March 2016. I told the Bank not to contact my mother again

The formal complaints process

In May 2017, on my return from New Zealand, I received a response to my complaint. NatWest acknowledged they were at fault and apologised ‘for any inconvenience caused’. NatWest also stated their willingness to return the money to my mother’s ANZ Bank account in New Zealand and to close the account. This turned out to be empty rhetoric. However, I provided all the required information about my mother’s ANZ account in New Zealand. I send the information via Post Office Track and Trace and received proof that it had been signed for on delivery. I repeated this four times over the next eight months.

RBS/NatWest continued sending my mother marketing material in New Zealand. My lack of trust in RBS/NatWest’s bureaucratic administrative system which lacked transparency, led me to ask that on closing the account they did not contact my mother again and that they remove her personal details from their records. I asked for this to protect my vulnerable mother from further anxiety and distress.

NatWest Bank sent me a second letter in June 2017 (the last letter from them) asking again for copy of my mother’s ANZ bank statement. I once again provided a copy of my mother’s ANZ Bank statement. As before I sent the letter by track and trace so that RBS/NatWest could not dispute delivery. I have done everything NatWest bank have asked of me, but they did not send the funds to my mother’s ANZ account in New Zealand. They did not respond to my letters. Only silence.

Involvement of the Financial Ombudsman

Whilst there was extensive rhetoric in RBS/NatWest’s letter of April 2017 with regards ‘unfortunate chain of events’ and an apology for their ‘error’ and ‘poor service’ etc, there was scant recognition of the considerable emotional distress caused to my mother and me. I did not believe RBS/NatWest would send the £3,372.21 to my mother’s account in New Zealand and in June 2017 sought assurance from the Financial Ombudsman that RBS/NatWest would be instructed to return the money to me or my mother. My view was that RBS/NatWest bank had miss-sold me a financial product i.e. a product that did not meet my needs. I also believed RBS/NatWest had breached the UK Banking Code and asked the Financial Ombudsman for that to be considered.

I received a reply from the Financial Ombudsman in August 2017. The Ombudsman adopted RBS/NatWest Bank’s perspective on all aspects of the case. The Financial Ombudsman did not consider whether the Banks had breached UK law and its own regulations by opening and activated the account without permission of the person named on the account.

The Financial Ombudsman did not follow up RBS/NatWest’s assurance to return the money to my mother’s account in ANZ Bank in New Zealand and the case was closed.

The Financial Ombudsman’s final statement was: As I’m not legally trained, I can’t look into legal aspects of a complaint. . . . ‘Unfortunately, it’s not within my remit to ask NatWest to amend its process or procedures. Therefore, given the circumstances I’m not going to ask it to do anymore.’ RBS/NatWest agreed with this statement and kept my mother’s money for its own use.

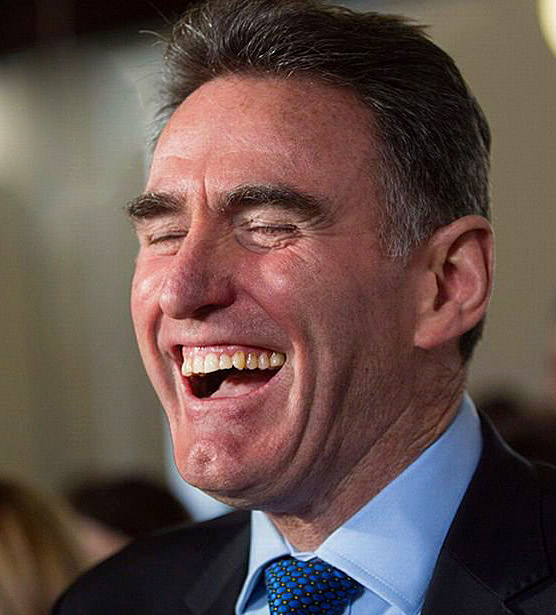

I wrote to Ross McEwan CEO of RBS/NatWest asking him to intervene since, like me, he had NZ citizenship, had two NZ daughters, and a mother residing in New Zealand. Also, as part of a marketing campaign he claimed that all his staff would’ treat customers fairly as though they were members of their own family’. He didn’t reply. RBS/NatWest were no longer replying to my letters and in October 2017 I made one final attempt at reconciliation. In the letter I stated: I have done everything in my power to provide you with the information you asked for in order that the money is returned. The letter was sent by registered mail, and I had evidence that it was received. Again, I did not receive a reply and the wall of silence remained in place.

The Small Claims Court.

In January 2017 I was surprised to receive an email and then a phone call from the Financial Ombudsman again. She apologised saying ‘I’m new to the job and poorly trained and out of my depth . . . I got it wrong . . . . I think the Small Claims Court is your best option now’.

So, since I had not heard from RBS/NatWest since June 2017, I was left with no alternative but to approach the Leeds Small Claims Court for a resolution otherwise NatWest Bank would keep £3,372.21 which is rightfully my mother’s.

My case rested on the belief that RBS/NatWest Bank had miss-sold me a financial product i.e. a product that did not meet my needs and had consequently breached the UK Banking Code. As claimant I asked that:

1). RBS/NatWest, should close the account, should not contact my mother again, and that they should remove her personal details from their records. I asked for this in order to protect my vulnerable mother from further anxiety and distress.

This sad episode caused my mother great anxiety and resulted in having to move to more secure hospital dementia unit. My mother’s future safety and well-being were my main priority in this case. RBS/NatWest Bank consistently refused to abide by the Data Protection Act. They placed her details on a general database, and the marketing department of the Bank sent letters to her offering loans and mortgages etc and that had to stop.

2), RBS/NatWest Bank return £3,372.21 to its rightful owner – my mother Mary.

3). RBS/NatWest Bank be instructed to pay Mary and me an additional £1,000. This was a token sum to reflect: the pain, suffering and personal injury to my mother and me; the costs of travelling to New Zealand to support my mother as a result of RBS/NatWest’s actions; and court costs i.e. £455.

I outlined our case against RBS/NatWest in a 9 page document to the Small Claims Court in Leeds supported by evidence for all the claims made. RBS/NatWest’s infamous Legal Division represented the case for the defence. From the very beginning they ignored rules governing Small Claim Courts practice. Their non-compliance with deadlines and procedures was not questioned by the court. The four-page RB/NatWest defence was written in legal jargon and procedural terminology which made it inaccessible to the ordinary person, No evidence was provided to support their defence. The final statement was: The court is invited to exercise its powers under CPR 3.4 or under its inherent jurisdiction to strike out the claim in its entirety, as it is totally without merit. This was surprising given they had accepted they were at fault. However, the court agreed and a 30-minute Preliminary Hearing was arranged for June 2017.

A couple of weeks before the hearing my mother’s bank in New Zealand informed me original sum of £3,372.21 leaving claims 1) and 3) remaining. For one year I tried and failed to contact the Mr Rose the local branch manager who filled out the form for opening an account in joint names who’d been sacked. I wanted him to be present at the court hearing as a witness but RBS/NatWest refused to provide any contact details or even forward a letter on my behalf.

The case was heard in a small untidy office in Leeds Magistrates Court. Deputy District Judge Barnes was presiding, RBS/NatWest were represented by a young female lawyer in a black professional outfit from London, and me, an old man, representing my mother. From the outset the Judge and the lawyer began conversing in technical legal jargon and there was much courtroom etiquette verbally “your honour”, and body language e.g. bowing, which made me feel an outsider in private club.

The RBS/NatWest lawyer slid a brown envelope towards me. I pushed it back. The Judge instructed me “You must take it” so I did. I read it at home. It was another four pages of defence, four pages of lies, deceit and innuendo. No evidence was provided. It was complete sophistry: the use of clever but false arguments with the intention of deceiving. The judge congratulated the lawyer with her concise ‘skeleton’ followed by more bowing and head nodding by the lawyer.

RBS/NatWest had ignored the rules in place to enhance transparency and fairness which stated: ‘Each party shall, at least 14 days before the date fixed for the final hearing, file and serve on every other party copies of all documents (including any expert’s report) on which he intends to rely at the hearing’. Of course, the judge was aware of this but would not let me speak in response -the judge had already based his decision on the first paragraph of this document, and nothing would change his mind. He ruled there was no case to answer in favour of RBS/NatWest. His reason was . . . and he read out the first paragraph of the ‘skeletal’ document:

‘It is Mrs A (Mary) who is the Bank’s customer. The Claimant (me) does not have a contractual relationship with the Bank, and the Bank has at no time owed the Claimant any duties, nor breached any duties’.

I calmly made two obvious points:

1) Technically I was a client of the Bank, holding two accounts with them, and my actions to open a joint account with the names of me and my mother were based on the Bank’s advice as a client, plus the advice of the Office of the Public Guardian The Bank had already admitted in a letter the mistake was theirs 13 months prior to the hearing.

2) I didn’t open an account in only my mother’s name – the Bank did. The Bank had opened an account without the permission of the person named on the account Mrs A ‘Mary’. Moreover, they falsely allowed money to be passed to the account which only the Bank had access to.

The Judge ignored these points, so I asked the next obvious question: ‘Isn’t it illegal to open an account with a person’s name without that person’s permission and then allow people to place money in that account knowing that only the Bank has access to that money for their own financial gain’?

He replied “Yes”. I couldn’t follow his logic and thought to myself ‘Does this set a legal precedent that Banks can open an account without a person’s consent and allow money to be paid into that account which only the Bank has access to’?

I asked the Judge if he would make it clear in his final ruling that the reason for ruling in favour of RBS/NatWest was: ‘It is Mrs A (Mary) who is the Bank’s customer. The Claimant (me) does not have a contractual relationship with the Bank, and the Bank has at no time owed the Claimant any duties, nor breached any duties’. The judge assured me he would and left the room. I subsequently received a letter from Leeds Magistrates Court stating the Judge had found in favour of RBS/NatWest and that the reason was ‘CPR 2.6 (1)(G). Since this ruling doesn’t exist the judge was able to hide the reason he relied on in court. The document also stated that I was refused leave to appeal by the judge. Without transparency there is no justice. Mary had been let down at every level. RBS/NatWest won because they had bigger teeth. It was one of the largest companies in the UK and had a legal team that attempted to deny liabilities for mis-selling products in the US brought by the US Government.

|

|

| Ross McEwan, CEO RBS/NatWest | Mary |

Postscript

I spoke to my mother’s nurse in the hospital wing of her Care Home in New Zealand a few months later. She said they had managed to block the numerous marketing material sent by RBS/NatWest but one had slipped through. She found Mary in bed crying – she was holding a letter from RBS/NatWest suggesting she take out Life Insurance – and she was deeply upset that she couldn’t do as they wanted because she had no money. My Mother died a few months later at the age of 95 years. At least she is in a place the RBS/NatWest Bank can’t reach her.